I’ve seldom witnessed a time when information was so unreliable.

We spend a phenomenal amount of time and resources focused on understanding what is happening around the world that may affect the stock market and other areas of our clients’ financial lives. We’ve always employed an intensely disciplined approach to review sources from various perspectives, comparing headline reports to primary sources of information, and doing our best to identify and challenge our personal biases. What seems crazy to us, is that nearly all of the information we come across, regardless of the source, has been wildly skewed and is propagandized to one side or the other. Naturally you’ll read this first as saying the other side is spreading misinformation, but it’s your side too.

Misinformation is baked into the data as well. We’ve again seen more substantive downward revisions of economic data, and it feels as though politicians and pundits have realized they can blast the most miniscule (and often irrelevant) information in memes across social media to manipulate public perspective. Again, all sides are doing this and if we truly want to understand the world around us, we must look first at the ways our own biases and groupthink can cause us to misinterpret reality. None of this is even touching the new reality that AI can fabricate all kinds of believable fakes (I’m not claiming everything is a deep fake, but I have access to AI video and audio tools, and it is alarmingly easy to do).

So what then, can we believe?

Businesses are run by people who are carefully working to create products and services for people who need them, and they aren’t doing it passively. They adapt to consumer demands, changing costs, new technologies, and economic conditions. They have a profit motive, and the end goal is to reward their owners in the form of a dividend payment. So, we invest by owning businesses that have been successful at this for many years. When we have a long-term perspective, these types of investments work very well and eliminate the need to obsess over market timing (which always hurts more than it helps).

It’s important to have the appropriate amount of cash in your portfolio. How much depends a great deal on your personal situation, but insufficient cash can force you to sell investments at a temporary loss that you otherwise wouldn’t sell. In our portfolios, we manage this dynamically depending on the magnitude of potential risks we see on the horizon (as those appear more significant, we tend to have more cash in portfolios). Having the right amount of cash in a portfolio also allows us to take advantage of opportunities as they arise.

We can diligently diversify risk across various industries, business, and service models while avoiding low-quality and high-risk investments (“index” investing really diversifies the high-risk, momentum stocks with lower-quality investments you wouldn’t intentionally buy). We can measure our effectiveness at this in a granular way and pay attention to the specific business, political, and economic risks that could hurt the business (tariffs are a great example here). A tariff on a specific product may heavily impact one business and have a negligible impact on a business not impacted by that product. Investments aren’t all the same, so it is important to invest in them on their own merits. For CoCreate clients, we fully manage this process for you.

We can believe that the only way we can fix the challenges in our society is to begin loving our neighbor, especially those who are different from us. We can’t expect the pundits and politicians to stop exploiting our polarized perspectives. We have to fix that on our own, in a grassroots groundswell of love, forgiveness, and humility. So as you’re watching headlines about anything going on in the world, remember that if you expect the worst from people, you’re guaranteed to get it, but if you open yourself up to look for the best in people, you’ll be surprised by how much you’ll find.

Military Operations in IRAN

I hate war, but I also hate mass murder. I’m confident nuclear weapons are destructive, especially in the hands of violent people. I’m amazed that the most dominant conversation around the conflict in Iran has been about gas prices rather than the millions of people tortured and murdered by the Ayatollah over the past 50 years. We should all feel the gravity of many conflicting emotions about the events that are transpiring. We are praying for every human life and for true peace when the conflict resolves. I will do my best to keep my comments focused on issues that will affect the market and economy.

While we have little quality information to rely on, there are several key premises we should be able to rely upon:

- The increase in oil prices is temporary; the end result of the conflict should result in a substantive decrease in the cost of oil coming from the region.

- This is not the same as Iraq/Afghanistan. If this turns into a protracted conflict spanning many years, the implications on the economy would be substantive. The current political climate, however, is not likely to authorize a declaration of war or provide funding for a substantial period of time. The constitution limits the President’s authority in this situation for 90 days. We project that in the most extreme case the conflict can’t survive the mid-term elections.

- Moreover, the stated intent and strategy of the military operation are vastly different from the campaigns in Iraq and Afghanistan. Dismantling Iran’s nuclear capabilities, seizing the enriched uranium, and toppling the Ayatollah are all objectives that can be achieved in a short time with little U.S. military presence on the ground. The strategy here is to equip the Iranian people to take back their country from a regime that is Stalin-esque.

- The Strait of Hormuz will be returned to international control, resulting in lower transportation costs for 20% of the world’s oil (net result, cheaper gas). Additionally, Saudi Arabia and other neighboring countries will build alternate transit routes to bypass the strait in case of a future closure. With the damage to Iran’s military and infrastructure, the United Arab Emirates will likely become the dominant player in Strait of Hormuz operations.

- We will see the Iranian people experience the opportunity to regain their freedom and perhaps become contributors to the global economy.

We are presently watching the start of a two-week ceasefire. The basis of the ceasefire agreement is unclear across various sources, and we are already seeing officials talking about where or not it has been broken. We would expect to see some of this in a cease-fire negotiation, but it underscores the reality that, from a market perspective, we must consider the conflict to be ongoing until peace is sustainable for the longer term.

Extended Bull Market and Slowing Economic Expansion

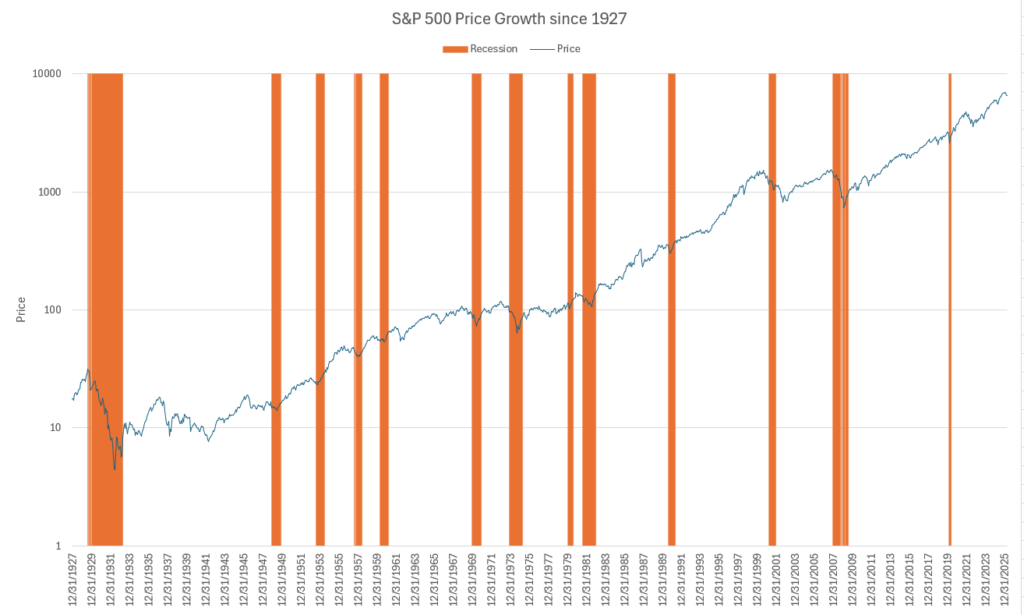

You can measure bull markets (growing stock market) and bear markets (declining stock market) in a variety of ways, and different commentators will mark the start and end of a bull market differently. In short, the stock market has been growing ever since the bottom of the great recession in 2009.

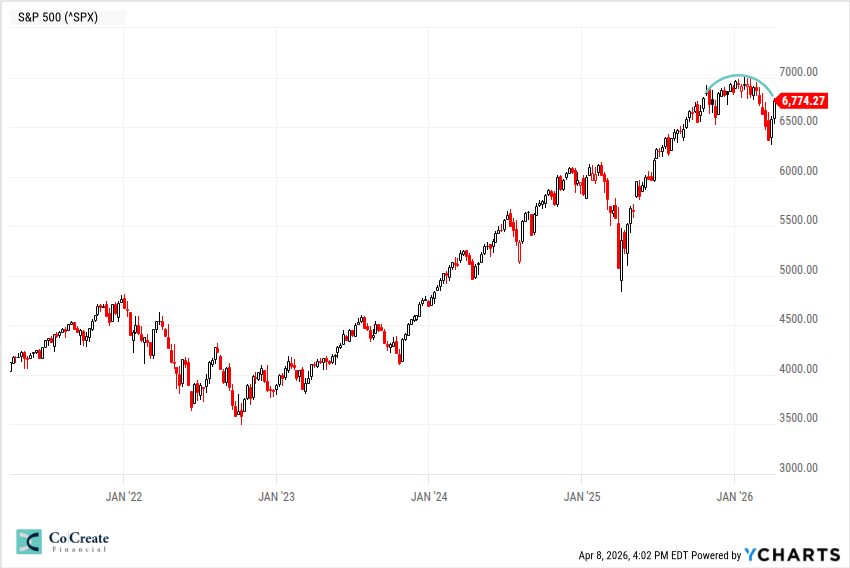

It’s been an exceptional bull market driven by a technological revolution that has changed life as we know it. These tend to last about 17 years before there is a meaningful correction in the markets. This isn’t a rule, of course, but we’re on year 17 and there are a mix of reasons to be excited about the future of the economy and things we should find quite concerning. In both cases, you want to be meaningfully invested in the stock market, because over time, these appear more like blips on the radar than financial catastrophes (they become catastrophic when you try to play them to your advantage. Inevitably, you end up selling at the worst time and buying back in when it’s too late). At the same time, we are becoming more defensive in our portfolios as many industry-specific risks and broader stock market risks increase. The S&P500 (which most people use to represent the “stock market” broadly… we think that’s fallacious, but that’s a conversation for another time), looks like it is beginning to form a rounded top. This tends to happen at the end of these secular bull markets as people begin to become concerned about the prospects of future growth. When we do this type of “technical analysis,” we need to be careful not to give it too much weight because it could mean something, it could mean nothing, or it could look entirely different tomorrow. As we are looking at the broader spectrum of data, it can sometimes be helpful.

The end of this secular bull market also doesn’t necessarily mean an impending stock market crash. There are many scenarios (some of which already appear to be playing out) which could avoid a broad-based market correction. We need to be strategic here, avoiding the major risks while maintaining well thought out investments in businesses that have a real basis for their value (i.e. healthy/growing profits combined with a long history of rising dividends).

Data Indicates Strain on the Economy

- Moody’s has estimated that the top 20% of earners have been responsible for 63% of the spending. These individuals are able to utilize profits from investments and real estate to buy more stuff… and more expensive stuff. The risk is that the “stock market” (different from our portfolios) has struggled this year, and if it doesn’t begin to grow, many of these top earners may start spending less.

- Additionally, consumer debt is less than exceptional. The New York Fed reports that 5.21% of auto loan balances are now 90+ days delinquent, the second-highest level since at least 1999 and above most of the 2008–09 financial crisis. Credit card delinquencies have climbed to 12.70%, the highest since 2011, while student loan delinquencies have jumped sharply as COVID-era repayment forbearance expired.

- Employment data is mixed.

Artificial Intelligence

We’re continuing to monitor the investment environment around Artificial Intelligence. In short, we’re still seeing an AI bubble. There is good and bad at this point (which is a slight improvement over only bad). The good news is that we are finally beginning to see AI implemented in ways that can yield significant productivity gains, while at the same time, protecting your own Intellectual Property and private data is becoming easier (I can train and run my own Large Language Model right on my laptop). As I see it, there are things AI will never be able to do, but things that AI can do exceptionally well. The most economically significant development at present is the ability to easily program custom solutions and/or integrations so that information and systems that have been cumbersome and fragmented can be accessed more efficiently across teams. I believe this will be the first wave of AI usage that creates widespread return on investment.

Despite the continued development of AI, the issues with investment in AI related business persist. Valuations (though AI stock prices have decreased, making values a little better than a few months ago), are still off the charts and demand massive new revenue to justify the current prices. The values are driven by a circularity problem with the major AI investors. JP Morgan analyst, Michael Cembalest, explained this issue clearly last October:

“Oracle’s stock jumped by 25% after being promised $60 billion a year from OpenAI, an amount of money OpenAI doesn’t earn yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (the equivalent of 2.25 Hoover Dams or four nuclear plants), as well as increased borrowing by Oracle whose debt to equity ratio is already 500% compared to 50% for Amazon, 30% for Microsoft and even less at Meta and Google. In other words, the tech capital cycle may be about to change.”

Essentially, there are massive investments being made by the big AI companies and reciprocal investments being made into the big AI companies, all without the support of any meaningful profit from the AI-related activities. It’s been massive corporate FOMO (fear of missing out). We still need to see enough revenue coming from AI business to justify investment in AI at the present time. Without that revenue, there is no basis by which we can expect anything but an AI crash.

Finally, the AI hyperscalers have been buying immense amounts of computing power (chips, data centers, etc.). Much of this will need to be replaced in the near future. According to McKinsey & Company, hyperscalers need to generate an additional $750 billion by 2030, just to account for the depreciation of this equipment. The combined profits of the hyperscalers are approximately $450 billion at present. These companies that are experiencing extreme values from the circularity issues also have a massive impending financial hurdle to overcome. Either the profits start showing, or the prices must come down much further so that they reflect these companies’ actual values.

Again, every business is not in crisis. We own many in our portfolios that are wildly profitable and are valued fairly (or even cheaply). We believe that now, more than any time in the past ~15 years, careful, intentional, long-term investment in profitable, dividend paying businesses matters. This simply can’t be accomplished by “index” investment, market timing, or many other common approaches. We are working hard to keep our client's portfolios profitable and prepared.