(406) 206-7571

Summary: Matt Hudak AAMS®, CFP®, CEPA®, Financial Advisor and Chief Investment Officer of CoCreate Financial, explains why the answer to whether you should roll over a 401(k) to an IRA (or a Roth 401(k) to a Roth IRA) is almost always yes, despite widespread internet misinformation driven by financial industry liability concerns and unresolved Department of Labor rollover regulation efforts stemming from Dodd-Frank. He compares 401(k)s as employer plans—limited investment menus, payroll-only contributions, vesting considerations, and stronger creditor protection—to IRAs, which offer far more flexibility, broader investment choices, consolidation of old accounts, and the ability to receive coordinated ongoing advice from a dedicated advisor. He notes potential downsides of IRAs if self-managed poorly, highlights myths about 401(k) fee advantages, and encourages viewers to evaluate rollovers in their specific context and seek professional guidance.

2026.05.08

Matt Hudak: Hi friends. We're going to talk about a really important question that a lot of people come to us with, and there's a lot of misinformation about it on the internet. The question is, should I roll over my 401(k) plan to an IRA? Or should I roll over my Roth 401(k) to a Roth IRA? What are the pros and cons? How do we unpack this? So we're going to dive in and talk about that in this video today.

My name is Matt Hudak. I'm the CEO of CoCreate Financial and really excited about this topic. When we look at this, a lot of the conversation, a lot of the information that you find online, has really centered around liability protection for the financial industry.

Back in 2012, when they enacted Dodd-Frank, they put in a directive for the Department of Labor to try to regulate rollovers, like they regulate the 401(k) plans even after they're outside of the employer plan. And this process of developing these regulations then has been caught up in court and in all kinds of different iterations of it that have been overturned, that have been thrown out, that have been really just not very functional. And so the industry as a whole has said, "we're going to say we're not going to give any advice on this. We're going to tell you it's better to leave it in the 401(k)," because that's the political risk that's on the firms to mitigate.

And they say, "I don't want to deal with violating a rule that doesn't exist yet." So they're more focused on that than really giving advice that's in the best interest of the person with a rollover, you.

So when we look at it, we want to look at a few different things. And we do need to evaluate this carefully in your context, but the short answer is almost always yes. You should roll over your 401(k) into an IRA. And there are a few reasons for that, but let's look at some of the differences and similarities before we dive into why you should.

One of the main differences with the 401(k) and the IRA is the 401(k) is an employer plan, and your IRA is your own plan, and that means a few things.

The IRA is very flexible. There's a lot that you can do in it. There's a lot you can do right. And in a lot of ways you can improve. There are a lot of ways that you can also go wrong and misstep in an IRA, especially if you're managing it on your own and, and you're not somebody that's built up the knowledge and experience with investing.

You can make a lot of unwise choices that maybe the 401(k) would prevent you from doing, but the 401(k) also, as an employer plan, has more limitations within it, and it has fewer different products that you can have. It also vests, which means that some of the money that your employers contributed as a matching contribution may or may not be yours yet while you're still working for the company.

Now, if you leave and roll over to an IRA while you're not fully vested yet, you might lose that vested amount. And then if you go back to work for that employer again, you might have to start over in that vesting schedule. And how that works is probably a great content for another video 'cause we don't have the time to dive into that here.

But when you're looking at that mix, you want to make sure that you're not planning to go back to the employer in the relatively near future because that could cause some problems to roll it over. If you're watching this video, you probably already know that you have to leave your employer in order to do that.

Or sometimes you might have that provision if you're getting ready to retire and you're in your sixties. You can sometimes roll over that balance to kind of get you started in the IRA and make your process of retiring more efficient. They call that an in-service distribution. And some plans offer that, some don't.

But within the 401(k) structure you have higher contribution limits, but you can only contribute through payroll. And the IRA, you don't have quite as high a contribution amount that you can make each year. But if you're not making the contribution to the 401(k) because you're not employed with that employer, you can't make that contribution anyway. So, the 401(k) has a higher limit of liability from creditors. So that you can't have a creditor when you owe money to someone, they can't come and collect that out of your 401(k).

In the IRA, you still have a million dollars of creditor protection. So it's still a substantial amount if we're looking at that IRA balance. But if there's a debt issue, we need to look at that and make sure that we're cognizant of what that looks like in our strategy for doing the rollover. Okay. So the biggest reasons to do this rollover really have to do with investments and advice. So when you're doing your research, you'll see online things about investment fees being different and maybe being less or negotiated down in the 401(k).

This is really just a myth. It depends on plan to plan. But often what we do see in 401(k)'s is that they have very low expense funds that are often low expense for a reason, they're subpar, their performance isn't great. And the quality of management is not very high. And the way that they get sales as a fund is to get them into 401(k) plans so that people have these limited choice menus and they'll buy these funds because it fits a category.

And a lot of times, employers or plan fiduciaries say well, I can meet my obligations by choosing something that's low cost, and they limit their search to things that tend to be low cost, and having a couple of things that are in a different investment mix, a different type of sector or, you know, something might be global, something might be small and aggressive or whatever.

And they pair a few things, but they tend to look at costs and other features of these funds. And we end up with these subpar mixes. They're just not portfolios that a professional investor would put together. They just aren't, and there's not enough choice within the 401(k) plans oftentimes to meet, even if they are good, to meet an investor's needs to meet one of our client's needs. So we're looking at saying, well, what do we do here? We want to be mostly in U.S. companies that pay dividends and there's not even an option in the 401(k) for that. Maybe we'll go with something that's the S&P500 index fund when we're investing in the 401(k) instead.

But then the S&P 500 index fund is not actually a diversified investment. It's 40% large cap tech stocks, which right now happen to be in a significant bubble as we're recording this. So that's actually a high risk momentum investment. And the 401(k) plans don't have the ability to account for those types of risks.

Whereas in the IRA, we can do a wide spectrum of things. Now, you don't want to go from a limited menu of investments that probably aren't going to get you into a lot of trouble. In your 401(k) plan to an IRA that you're managing and maybe doing highly speculative things like investing in Bitcoin.

Or there are some ways that you can own real estate in IRAs that have some pretty massive logistical drawbacks that create a pretty intense risk for you if you're not very very methodical in how you've evaluated that. So there are things that you can do again to misstep in these IRAs if you are not careful, if you're managing them yourselves, especially because if you're working with a professional, they should know the things that are going to cause problems and be aware of those and how to avoid those things. But within that spectrum, within an IRA, you can also own dividend yielding stocks. You can own tech stocks, you can own bonds, you can own individual bonds, you can have funds, you can have ETFs, you can have really any kind of investment that's out there in some form.

And there are a few things that are outside of that scope, but they're not mainstream types of investments that you can't own inside an IRA. So you have a lot of choice and a lot of ability to manage this in a way that works and you can hire professionals to get ongoing advice and to really have a financial plan that's coordinated to meet your needs.

Whereas in the 401(k), some of them do now have like a one 800 number where you can call a certified financial planner professional to get some advice on what you're thinking. But that person that you're calling doesn't really know your situation, like a financial advisor that you're hiring that's in your community, that's engaged with you, that knows your kids' names and knows how long you've been married, that understands the community, the type of neighborhood that you're in, where you're going, what your business looks like, that knows your tax situation, your estate plan.

So you don't really get the same kind of advice in a 401(k) that you can get outside of that 401(k) when you're working with a professional advisor that's dedicated to you and has an ongoing engagement. And then the other thing is with IRAs, you can roll over your 401(k) from the job that you just left into an IRA.

You can roll over the 401(k) from the job you left 10 years ago into the IRA and you can keep your investments consolidated. And sometimes you can even save in other types of buckets, like other types of accounts. We talk about these things like buckets here at our firm 'cause we like to be simple and speak in plain English, but you can put it into an account that you can save in parallel to the IRA too.

You can save where you can access it before retirement. So there are lots of different things you can do, but you can keep everything in one place. If you do these rollovers, and you're not going to walk into your retirement era in life or your next chapter and say, “I don't know where all my money is. I know I had this 401(k) from this old job, but I don't know how to find it.” That's a common thing. Or you'll be coming in and saying, I found this 401(k) from 30 years ago that I didn't know was just sitting in cash and could have quadrupled over the 30 years or whatever it would be in value. Again, that's not guaranteed, right.

Performance has risks and all of those things, having an investment grow, but you didn't realize that it was sitting there in cash or maybe even an unclaimed property somewhere. These are common things that we encounter with people is that they've lost assets from the past and it actually has a significant negative outcome for the client. When we see those things happen, in most cases, sometimes you find a hundred thousand dollars and you say, that's pretty sweet that I just realized I had this money that had been growing since I was 22. And that was like that, that's awesome. But that's the uncommon side of it.

More often it's things weren't managed appropriately because you forgot about them. And so keeping things consolidated, keeping things in a place where you can get professional advice really has a dramatic advantage. And most of the information that you see on, you know, the pros and cons of doing a rollover are really oriented around satisfying this regulatory burden and the liability that's been put on the financial industry to try to tell you you should keep money in the 401(k)s because they don't really want to say roll it over and then find out that they had some requirement that they didn't check on a form or something like that down the road. So there's really been really poor advice on this over the last 15 years or so. So I really want to encourage you to think about that. The fees are generally very similar.

Anything can be compared. It's apples and oranges. You might spend a little bit more on one side or the other in a specific context. But compare all these things, get advice, reach out to us. We're always happy to talk to you about the actual implications of your decision and what that means and help you make that decision from a really grounded, rooted, wise perspective. I'm excited to talk with you about this. Give us a call. We're always available to help you make these decisions. And excited. Take care.

Summary:

Matt Hudak AAMS®, CFP®, CEPA®, Financial Advisor and Chief Investment Officer, and Christa Hudak CFP®, ChFC®, CKA®, Financial Advisor and Chief Planning Officer for CoCreate Financial, explain their approach to financial planning by aligning financial decisions with a client’s core values, beliefs, and convictions to create more long-term satisfaction than traditional math-only goal setting.

2026.05.07

Christa: Thank you for joining us today. I'm Christa. And this is Matt. And today we're going to be talking about how we approach helping you align your financial planning, your financial decision framework with the values that you hold dear, and how and why that's important to make you truly successful in the long term.

Matt: Yeah, and what we found is when you do this, you really have a lot more satisfaction in your outcome across the board. We've spent a lot of years kind of following a traditional approach to thinking about financial goals that's really just purely math based.

And what we found is that it doesn't really lead you to the most efficient outcome in terms of what you internalize. Oftentimes people are not saving enough and they feel afraid of the future, or they're saving too much.

And they're afraid to spend it when they really should be using that for something that's meaningful 'cause you can't take it with you.

Christa: And I'll just add like these conversations that what we're going to get into, they're where things really come alive and they're the hard part, because if you were to say, you know, I want to buy a house that's worth this much in this many years, that's just a math problem. That shouldn't be hard for us to figure out.

Especially as financial experts who can run the time value of money calculations. That's not a hard question. The hard question is "how do we get the goals right and how do we line this up well over time?"

Matt: Yeah. And when we're looking at this, we look at a few different things and traditionally this has been like we've talked about math-based calculations to say how much are you going to have when you're long gone? And how do you make it last for forever? And then just give it this pile of money to your heirs. And hope that they do things well with it that they live well, maybe even in a way that you didn't. And what we look at is there are really three different types of capital that we have to plan for at the same time.

The first one of these is your financial capital, and that's pretty obvious. It's your money, it's your debt, your assets, your house, your cars, your cash, your stocks, all the different things that you own. Your business, if you have a small business. This is your financial capital. It's the stuff we can measure and calculate.

We have to make a plan for that. We have to make it last. We have to help you deploy that in the present as well. The next thing that we have is your social capital. This is really your influence. This is the influence you have in your family, in

Christa: your community,

Matt: in your community, in your church, in your business, with your employees, with your employers. You have influence across a wide range of individuals.

How do you make the most of that? How do you impact those people personally? How do you leverage that as well to have more impact in your community and to live a life that's more fulfilling in your sphere based on your beliefs and values and convictions, which we'll talk about that a little bit later.

And the third type of capital that we have is sorry, I already said social capital, spiritual capital. And this is, what are the lessons these deeply spiritual things, that you want to pass on? What are the beliefs that you think are important that have shaped who you are? These look different for many of us. Our spiritual capital is very significant in our lives. We really value our spirituality and our faith, and it's a main driver for us. And we find that's true for most people of faith. But even if you're not a person of faith, you have this spiritual capital. How do you want to influence people on that deeply personal and spiritual level and shape those people?

What are those things that you can give? So when we're looking at these we don't want to save these up until you're gone. If you look at things like social capital, spiritual capital, it's really easy to see that it doesn't do any good if you just wait until you've passed away, and you've never been kind to anybody, or never cared or showed up for somebody, and you write them a letter after you've passed and say, you know you're going to receive this when we're at my funeral. It doesn't do anything. Right. It's obvious to us that those you can't pass after the grave, but financial capital is also something that you need to distribute and balance over the course of your lifetime. We don't want to see any of our clients starve in retirement, but we also want to make sure that our clients are able to live here and now and do the things that are meaningful and impactful all along throughout the course of their life.

Christa: And also, when we encounter people that have excess, you know, they've been good savers, they don't have extravagant lifestyles, and we're looking at the situation and there is in fact excess, we want to give them the opportunity to ask the question, how do I want to use this or distribute this during my lifetime, instead of just saying, well, they're happy with living on a lot less than their portfolio can generate, and it'll just go into their estate. But to give them that opportunity in the present as we assess things to say, what do you think the best choice of using this money is?

Matt: And it's a lot more fun to take that approach. So we really hope that we can engage these different types of capital along the way. And we use a values and beliefs filter to really help identify how that works.

Christa: Yeah. So kind of shifting to another place in this diagram that we'll have up on the screen, we have these concentric circles, and in the financial industry we tend to live on the outside of the circle and we want to talk about things like, you know, what's your family situation? Are you married? Do you have kids? Who are the people involved here? What do you do for work? How much do you pay in taxes? What other components are things that we need to fund or things that interact with the finances? And we tend to live just in that outside sphere of conversation. But what we find is that to really understand those things for our clients and to really drive forward on a holistic plan, we have to start at a much more core level, which is, what are your beliefs, values, and convictions, and how do those drive the things that are most important to you?

Matt: Going from that tangible outer circle to sort of almost through the circle that defines our passions to what's really at the core of those.

Christa: Yeah, absolutely. Because we find that this changes things and it also helps explain the things that are most important to us, and also filter out the things that maybe are not so important, and we can all come up with all kinds of goals, right?

And 'cause so often we just say, well, what do you want? And you're like, well, I can start spitting off some things that I think would be cool. And if you really lean into those, you'll decide that they're really important, and maybe they are.

But if we don't ask the question of why they're important, we can find ourselves going in the completely wrong direction.

Matt: Yeah. And whether those are career goals or recreation goals, travel types of goals that might be family, a family vision that you have, as we ask those questions of, well, what's driving behind that?

What's the driver behind that? What's the why? We have to do that even sometimes a few times.

Continuously. Yeah, continuously. And really, really dig. Dig down deep to say, you know, what are the pieces that aren't changing about this?

You know, when you get to the place of having that new house, what's still the same because once you get to your dream house, you have to figure out the next chapter and reinvent yourself. You have to have a new vision and a new dream. So there's something that has to be really more centered to align all of your goals so that you can be consistent and really achieve those things.

And one of the things I think that we found is a lot of these values, these beliefs, these convictions, these things that are core to our ourselves, they actually don't take a lot of capital.

They're often free.

Christa: Okay.

Matt: If you really care about having a healthy marriage, if that's a value to you that doesn't take money. Sure it's nice to go out to dinner or it might be nice to take a vacation with your spouse or do something. That's not to say that money can't add value. Your resources, if they're used well can bring some satisfaction to those, especially temporally.

But you know, in our marriage, we're married, by the way, if you don't realize that already. But in our marriage we get to spend time with each other. We get to work on our communication skills and we get to pay attention and actually look internally and say, am I valuing Christa? And that doesn't take anything. That's free for me to build good habits in our marriage and to pay attention. So, a lot of these beliefs and values and convictions that we find people have they don't take a lofty savings plan to get there to accomplish it. It's really about being disciplined and focused on the things that matter in the present, and then allowing the resources and the ways that you're using the capital to augment those and amplify your ability to be successful in those things.

Christa: Absolutely. And the other reality that we face is that goals are simultaneous, not sequential, and often in competition with each other. So, one of the things that comes up a lot that we see all the time is, you know, we'll have business owner clients who will have ideas or want to go on new ventures for growing their business, and they're really excited about those opportunities within their business.

And then they'll also say in the same conversation, and I want to spend more time with my family. And those are both very good things to be growing your business and spending time with your family, but sometimes they're in conflict with each other and that's just the reality of it. And there's no one size fits all answer to how to divvy that out or how to make that work.

But, to be honest, where we have to say we hold these values, and to get really real about what those are and what the most important things are, what the most important things are in different seasons, and be willing to say, okay, these values exist. These are the different things that I want to do. How do I align these up so that both can be accomplished when there is this tension of, you know, one seems to infringe upon the other?

Matt: And how do you reconcile that? To riff off that example, you might have a business idea that has a really positive impact in your community and that might be really, really important to you. And that might align with your values of having a really positive community impact of kind of, hopefully it's a little more specific than that 'cause that's pretty generic. But so you're looking at that, but you're also saying, I want to be there for my kids at this stage. Those are both really important and good things, and you might lean toward solving that in some sort of chronological prioritization structure. Or you might prioritize that by impact and say, well, I am going to go into work on the community impact and hope that's a good example for my kids.

That's social capital and spiritual capital that you get to distribute by giving a good lesson for your children. Or it could be I'm going to find a way to bring my kids along in that impact. And there are different ways that you can arrange that, but without identifying both the tension and then the value drivers behind them, you can't really reconcile those very well.

We find that this values alignment has so many different dynamics that it brings. Spending problems, those are usually heart condition problems. Those are usually, I want some to satisfy something that I don't feel like is being satisfied right now so I'm going to look at a thing to meet a need that I have that's really intrinsic.

And we get into these habits of overspending. We see marriages where people come in and they're not in alignment and they're having trouble talking about the finances. Well really, if we get these values alignment issues figured out, if we get them on the same page as one another on these core things, then the financial pieces start to fall into place a lot more easily.

And so we're able to work through those issues too. So this is a really powerful tool as we're going through and looking through this with people. We're really, really excited about the opportunity to walk through some of this journey with you. It takes a lot of work, it takes a lot of time.

We don't get to discover these things overnight about the people that we're working with. It's a long process of asking those why questions. So, we're really excited to explore this with you and to sit down and talk through these things, figure out what your financial capital looks like and your social capital, your spiritual capital, these beliefs and values and convictions, how these can drive your purpose, your impact, and lead you to a far more satisfied end result in your financial life as you go through your whole financial life.

So we look forward to meeting you here in our office and talking through this more.

2026.04.10

Christa Hudak: Hi friends. My name's Christa with CoCreate Financial, and today I want to talk to you a little bit about the issue of overspending, and we're going to talk about it from a little bit of a different angle. But first, let me set this up for you, because as a financial advisor, I have the opportunity to engage with a lot of different people in a lot of different scenarios.

And there are some really interesting things that emerge, especially as we look at the concept of overspending and what that can look like in different scenarios. And I first want to start on the positive side, which is that I encounter a lot of different individuals at all different income and asset levels who are very content and do not overspend. It is truly incredible to me. Sometimes I encounter people with very, very modest incomes who don't feel like they need anything more, and often are saving significant amounts. And I have other clients who have significant resources and lots of income who who manage that very well.

And so we see people successful in their spending levels at a huge range of income levels. On the flip side, we see something very similar with overspending. Um, And this can look like accumulating consumer debt or maybe even just spending at a level that you're always a little bit behind. You know, maybe you don't have a mounting consumer debt issue, especially at those higher income levels.

But maybe there's nothing to save and even small things that throw you off financially and small little emergencies, like needing to fix your car, become a big thing because you don't really have any reserves, even though there's a significant amount of income. And what's interesting is that there's no income level where these things disappear and it's really easy to you know, take a look at your budget, take a look at your spending and say, hey, all I need is $500 more a month, or I need a thousand dollars more a month. But we consistently see when people have a spending problem that the increase in the money doesn't fix it. And that really should give us pause and say, what's really going on here?

Because if it was as simple as, you know, this amount of money is not enough. I just need a little bit more, a little bit more money should fix it. But that's never what happens outside of a different strategy. And that's why I want to posit to you today that an overspending issue isn't actually a math issue.

It isn't actually an issue of how you're organizing your finances necessary, though, that can definitely help and that can bring these things to light. The real issue is actually a heart issue, and it's a condition of what you're longing for and what you're chasing. So let's unpack that a little bit more.

When you are overspending, it's because you're desiring for something more and you're not connected with what's really going to bring you fulfillment. And so you're always looking for that in financial means, which is a pretty radical statement to say that it's not just as simple as I need more money and that's going to fix it.

But we know that can't be the answer because people continue to overspend even as they have significantly more money. So with this, if this is something that you're struggling with, no matter where you fall on the income spectrum, I would just encourage you to you know, first of all, do the due diligence.

There are so many, so many resources about managing a budget and not overspending. Do those things to evaluate what you're spending and how you're spending it, but then to ask the questions of what's really behind this? And why am I unsatisfied? What's going on in my heart, in my relationships, in my situation, that is driving my desire to spend money on things that I know I can't afford?

And to reorient yourself because this is not an issue that's just going to go away. It's not going to get fixed with making more money, and it actually gets a lot scarier as you make more money because you know when, when you're living on a modest income and overspending, you're going to have this mounting credit card debt, and that can is obviously very, very problematic.

But something happens as you get into higher levels of income, which is that lenders will give you even more. And more and more. And those things can snowball really quickly into actually significantly worse situations and more difficult situations to get out of. So I would just encourage you to ask this question, what's really going on?

And you know, if you're married, have a conversation with your spouse and start unpacking. The truth of why you are struggling with spending and that, and the recognition that it's not a simple math problem, it's something going on on a much deeper level. I hope this is helpful for you today and encourage you to just take the time to reflect.

I’ve seldom witnessed a time when information was so unreliable.

We spend a phenomenal amount of time and resources focused on understanding what is happening around the world that may affect the stock market and other areas of our clients’ financial lives. We’ve always employed an intensely disciplined approach to review sources from various perspectives, comparing headline reports to primary sources of information, and doing our best to identify and challenge our personal biases. What seems crazy to us, is that nearly all of the information we come across, regardless of the source, has been wildly skewed and is propagandized to one side or the other. Naturally you’ll read this first as saying the other side is spreading misinformation, but it’s your side too.

Misinformation is baked into the data as well. We’ve again seen more substantive downward revisions of economic data, and it feels as though politicians and pundits have realized they can blast the most miniscule (and often irrelevant) information in memes across social media to manipulate public perspective. Again, all sides are doing this and if we truly want to understand the world around us, we must look first at the ways our own biases and groupthink can cause us to misinterpret reality. None of this is even touching the new reality that AI can fabricate all kinds of believable fakes (I’m not claiming everything is a deep fake, but I have access to AI video and audio tools, and it is alarmingly easy to do).

So what then, can we believe?

Businesses are run by people who are carefully working to create products and services for people who need them, and they aren’t doing it passively. They adapt to consumer demands, changing costs, new technologies, and economic conditions. They have a profit motive, and the end goal is to reward their owners in the form of a dividend payment. So, we invest by owning businesses that have been successful at this for many years. When we have a long-term perspective, these types of investments work very well and eliminate the need to obsess over market timing (which always hurts more than it helps).

It’s important to have the appropriate amount of cash in your portfolio. How much depends a great deal on your personal situation, but insufficient cash can force you to sell investments at a temporary loss that you otherwise wouldn’t sell. In our portfolios, we manage this dynamically depending on the magnitude of potential risks we see on the horizon (as those appear more significant, we tend to have more cash in portfolios). Having the right amount of cash in a portfolio also allows us to take advantage of opportunities as they arise.

We can diligently diversify risk across various industries, business, and service models while avoiding low-quality and high-risk investments (“index” investing really diversifies the high-risk, momentum stocks with lower-quality investments you wouldn’t intentionally buy). We can measure our effectiveness at this in a granular way and pay attention to the specific business, political, and economic risks that could hurt the business (tariffs are a great example here). A tariff on a specific product may heavily impact one business and have a negligible impact on a business not impacted by that product. Investments aren’t all the same, so it is important to invest in them on their own merits. For CoCreate clients, we fully manage this process for you.

We can believe that the only way we can fix the challenges in our society is to begin loving our neighbor, especially those who are different from us. We can’t expect the pundits and politicians to stop exploiting our polarized perspectives. We have to fix that on our own, in a grassroots groundswell of love, forgiveness, and humility. So as you’re watching headlines about anything going on in the world, remember that if you expect the worst from people, you’re guaranteed to get it, but if you open yourself up to look for the best in people, you’ll be surprised by how much you’ll find.

Military Operations in IRAN

I hate war, but I also hate mass murder. I’m confident nuclear weapons are destructive, especially in the hands of violent people. I’m amazed that the most dominant conversation around the conflict in Iran has been about gas prices rather than the millions of people tortured and murdered by the Ayatollah over the past 50 years. We should all feel the gravity of many conflicting emotions about the events that are transpiring. We are praying for every human life and for true peace when the conflict resolves. I will do my best to keep my comments focused on issues that will affect the market and economy.

While we have little quality information to rely on, there are several key premises we should be able to rely upon:

We are presently watching the start of a two-week ceasefire. The basis of the ceasefire agreement is unclear across various sources, and we are already seeing officials talking about where or not it has been broken. We would expect to see some of this in a cease-fire negotiation, but it underscores the reality that, from a market perspective, we must consider the conflict to be ongoing until peace is sustainable for the longer term.

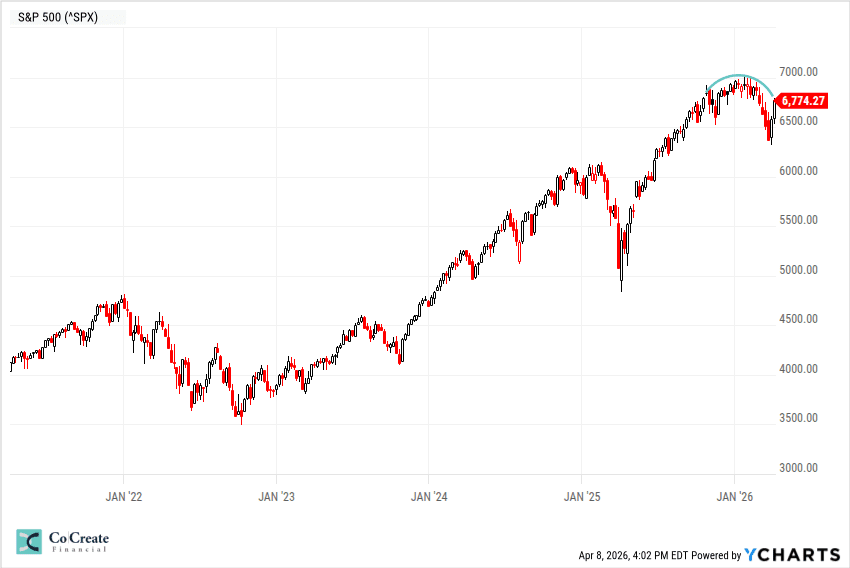

Extended Bull Market and Slowing Economic Expansion

You can measure bull markets (growing stock market) and bear markets (declining stock market) in a variety of ways, and different commentators will mark the start and end of a bull market differently. In short, the stock market has been growing ever since the bottom of the great recession in 2009.

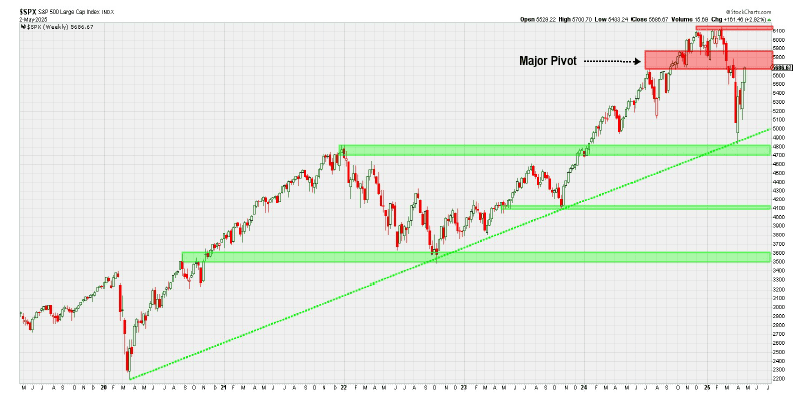

It’s been an exceptional bull market driven by a technological revolution that has changed life as we know it. These tend to last about 17 years before there is a meaningful correction in the markets. This isn’t a rule, of course, but we’re on year 17 and there are a mix of reasons to be excited about the future of the economy and things we should find quite concerning. In both cases, you want to be meaningfully invested in the stock market, because over time, these appear more like blips on the radar than financial catastrophes (they become catastrophic when you try to play them to your advantage. Inevitably, you end up selling at the worst time and buying back in when it’s too late). At the same time, we are becoming more defensive in our portfolios as many industry-specific risks and broader stock market risks increase. The S&P500 (which most people use to represent the “stock market” broadly… we think that’s fallacious, but that’s a conversation for another time), looks like it is beginning to form a rounded top. This tends to happen at the end of these secular bull markets as people begin to become concerned about the prospects of future growth. When we do this type of “technical analysis,” we need to be careful not to give it too much weight because it could mean something, it could mean nothing, or it could look entirely different tomorrow. As we are looking at the broader spectrum of data, it can sometimes be helpful.

The end of this secular bull market also doesn’t necessarily mean an impending stock market crash. There are many scenarios (some of which already appear to be playing out) which could avoid a broad-based market correction. We need to be strategic here, avoiding the major risks while maintaining well thought out investments in businesses that have a real basis for their value (i.e. healthy/growing profits combined with a long history of rising dividends).

Data Indicates Strain on the Economy

Artificial Intelligence

We’re continuing to monitor the investment environment around Artificial Intelligence. In short, we’re still seeing an AI bubble. There is good and bad at this point (which is a slight improvement over only bad). The good news is that we are finally beginning to see AI implemented in ways that can yield significant productivity gains, while at the same time, protecting your own Intellectual Property and private data is becoming easier (I can train and run my own Large Language Model right on my laptop). As I see it, there are things AI will never be able to do, but things that AI can do exceptionally well. The most economically significant development at present is the ability to easily program custom solutions and/or integrations so that information and systems that have been cumbersome and fragmented can be accessed more efficiently across teams. I believe this will be the first wave of AI usage that creates widespread return on investment.

Despite the continued development of AI, the issues with investment in AI related business persist. Valuations (though AI stock prices have decreased, making values a little better than a few months ago), are still off the charts and demand massive new revenue to justify the current prices. The values are driven by a circularity problem with the major AI investors. JP Morgan analyst, Michael Cembalest, explained this issue clearly last October:

“Oracle’s stock jumped by 25% after being promised $60 billion a year from OpenAI, an amount of money OpenAI doesn’t earn yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (the equivalent of 2.25 Hoover Dams or four nuclear plants), as well as increased borrowing by Oracle whose debt to equity ratio is already 500% compared to 50% for Amazon, 30% for Microsoft and even less at Meta and Google. In other words, the tech capital cycle may be about to change.”

Essentially, there are massive investments being made by the big AI companies and reciprocal investments being made into the big AI companies, all without the support of any meaningful profit from the AI-related activities. It’s been massive corporate FOMO (fear of missing out). We still need to see enough revenue coming from AI business to justify investment in AI at the present time. Without that revenue, there is no basis by which we can expect anything but an AI crash.

Finally, the AI hyperscalers have been buying immense amounts of computing power (chips, data centers, etc.). Much of this will need to be replaced in the near future. According to McKinsey & Company, hyperscalers need to generate an additional $750 billion by 2030, just to account for the depreciation of this equipment. The combined profits of the hyperscalers are approximately $450 billion at present. These companies that are experiencing extreme values from the circularity issues also have a massive impending financial hurdle to overcome. Either the profits start showing, or the prices must come down much further so that they reflect these companies’ actual values.

Again, every business is not in crisis. We own many in our portfolios that are wildly profitable and are valued fairly (or even cheaply). We believe that now, more than any time in the past ~15 years, careful, intentional, long-term investment in profitable, dividend paying businesses matters. This simply can’t be accomplished by “index” investment, market timing, or many other common approaches. We are working hard to keep our client's portfolios profitable and prepared.

2026.03.16 Podcast Episode 2

Matt Hudak: Hi friends. My name is Matt Hudak. This is Christa Hudak. If you haven't had the chance to meet us, we're really excited that you are exploring CoCreate Financial and checking in on how we invest. That's what we'll be talking about today in our video. Just a little bit about our investment philosophies, how we approach each client's asset allocation, all those different things.

I promise we'll do it in plain English and it should make a ton of sense and hopefully inform your decision and our exploration process so that when we connect in person, we're able to focus more on the specific questions that you have, and less on just us talking at you about investment things that you probably don't even care about all that much.

So we're going to dive in and kind of talk about how we structure this.

Christa Hudak: Before we get into the specifics of talking about investments, the first thing we want to take a step back and consider is how we view a financial picture and making sure our clients have a setup that leads to [00:01:00] their financial freedom.

And when we do that, you know, the very first base level that we always make sure with all of our clients is that they have appropriate cash reserves and then we bucket their assets. And this works both from the standpoint of cash management, of cash flow management, of just your regular income and also with your investment assets and how we approach it.

And we have this graphic that will show up on the screen as well that's something we use as we have this exploration for everyone. And the first thing that we always want to consider is that your basic needs are being met, right? So that you're paying your mortgage, you're able to eat reasonably, you're covering all the necessities in life.

And this is, like I said, true both for cash flow and then also when we're doing long-term planning and retirement planning, is that we really want to protect the chunk of your assets. And pay special attention that your basic needs are met throughout your life. But the reality is [00:02:00] everybody, most everybody wants something a little bit more than just the bare minimum.

And we call that your adventure bucket. And this looks different for different people. Maybe it's living in a little bit nicer of a house or going out to eat or travel plans or all kinds of extravagant, fun things that we enjoy in life.

Matt Hudak: Yeah. It's the extras.

Christa Hudak: Yeah. That you're like, oh, I don't need this to live, but this is the thing that makes life fun.

And so we want to make sure we cover your basics. And then we also want to make sure that we're covering things that accomplish the things that you want to do in life. And somewhere in that range, there's what we call like enough. Sometimes people will talk about it as like a financial freedom line or a financial finish line of this recognition of, hey, I can be content at this level and satisfy the things that really matter to me, but that doesn't mean that that's all that there is to do, or maybe you have resources that exceed that. And so sometimes there's more adventure to be had. And then we also look at this idea of an [00:03:00] impact bucket. And this can be the crazy projects or maybe it's a lot of gifting to family members or maybe some generosity of charitable giving.

Matt Hudak: Yeah, it might be pursuing business growth, a lot of those different pieces. So what does that look like in terms of when we're looking at somebody's assets, how much do we typically see in terms of need with that, like covering the basics to produce income, to cover your basic needs, what might that adventure bucket then look like beyond that?

Christa Hudak: Well, to be completely honest, this is very unique for everybody because we see a wide variety of just lifestyles and what people engage with and also different setups in it. There's different components in this that adjust those numbers both from the standpoint of what you are going to consume from it.

Maybe you just tend to live a simpler lifestyle and are very content with that. Or, also other income that comes in. So depending on what social security income looks [00:04:00] like, or if somebody has pension income. The needs for those assets in that bucket to cover the basics goes down, but typically we see the basics and a little bit of adventure included when we have clients in the one to two million range with some additional income like we talked about. That's pretty typical.

Matt Hudak: Awesome. Yeah. And we'll fund that basics bucket typically with a portfolio of you know, dividend yielding stocks. We might fund that with some fixed income. We'll talk about what those things are in just a moment, but we'll look at really liquid, really secure things within the adventure bucket.

We'll probably look at more things like real estate rentals, those types of investments, they might be really stable income, except they've got some concentrated risk. You know, something goes wrong and the tenant doesn't pay. It's a big hit. So it's like they work well, but when they don't work, they really don't work for a period.

So we don't want to take those risks with your basic needs. But some of the adventure bucket, those [00:05:00] things kind of come into play there. And then in the impact bucket, we're looking at private equity and some impact investing sometimes like that. Things that can really do good in the world, solve hunger problems or human trafficking issues and make a profit at the same time.

So we look at all those different pieces but as you go up in those tiers, across those buckets, you have the ability to take some more strategic risks to accomplish great things because you're not needing those. But we also want to protect what you really need. So when we're doing that here's kind of what it looks like. There are a couple fundamental philosophies that we really hold to. We take a very business-minded approach to how we invest. So when you're looking at an investment with us, what we're doing is we're thinking about it like the business that we own.

The business that you, if you're a business owner and you own a business, we're thinking about the same way you would think about buying an individual business or making an individual loan or doing something like that. We make sure that we're really making smart decisions. The second thing that we've done is we've really taken a philosophy that clears [00:06:00] away a lot of the clutter from the complex investment products and the investment theories that really haven't added a lot of value to our ability to create returns in a portfolio.

They've added a lot of complexity. Some of them have added things that actually create new problems that we didn't have to deal with before, those types of theories. So we really take a very clean and simple approach that makes a lot of business sense.

Matt Hudak: And then we use a discipline process with that, and it allows us to maintain a laser focus on every investment that we own across our whole entire client asset base. And it actually allows us to measure things like diversification. It used to be that diversification was just owning everything and seeing what worked and what didn't, and you just kind of offset different types of things very generally, and it was a very kind of shorthand approach.

We take a very focused strategic approach where we can put numbers to this, and we audit that every month and debate that and discuss that as a team to make sure that we're appropriately managing our [00:07:00] client accounts at an investment level, at a very granular level, and we can specifically evaluate because of that, the specific business risks, the specific investment risks that exist with each investment, rather than just trying to monitor, you know, up and down fluctuation at the pricing in your account.

What's the actual risk that you have in that investment? What's the actual reward and how do we mitigate those strategically on a one-on-one level with each investment?

Christa Hudak: So Matt, do you want to back up and kind of show us how we view investments at their core?

Matt Hudak: Yeah, absolutely.

And we'll focus if it makes sense, we'll focus on just kind of this basics bucket, this more liquid style. When we get into the individual real estate properties, the private investments that someone might make, those are so individualized and they're so different from one to the next that we have to take a very focused approach in the context of our meeting, if that's you, but the first couple million dollars, like where we went, we were talking about will be in this basics bucket. So I'm going to go [00:08:00] ahead and pull up a whiteboard here and share this with you.

And kind of go through how we think about investing in general. So when you are making investments, it's not really owning markets or indexes or averages, it's not complex. It actually boils down to two things and there's kind of a third. That's the real estate side of things, but it fits kind of into the business ownership concept that we'll talk about.

The first thing that you can do is make loans.

I'm going to hold this because it's bouncing a little bit. So you can make loans and the other thing that you can do is you can own businesses. Own businesses. There we go. So when you're making a loan to somebody, I want you to think about this a lot like you're lending money to a friend. If you've done that at some point, or maybe even somebody that's not a friend, a random [00:09:00] stranger, I don't know, that's one of the questions you have to ask.

If you're making this loan, think about what you're going to ask this person that you're lending to. You know, do they have a source of income to pay it back? What's the loan for?

Christa Hudak: When do they say they're going to pay it back?

Matt Hudak: Yeah. When do they say they're going to pay it back? Are they going to pay you interest?

Have you ever lent them money before? What do they do with it? Did they pay you back? All these questions we evaluate when we're looking at making loans as an investment. The only difference is you're making these investments to usually large corporations, governments and you're evaluating that on a case-by-case basis.

It's very different to make a loan to the city of Detroit than it is to the United States government than it is to Nigeria or to Coca-Cola. So it just depends on that mix. And we have to ask these questions. So what happens when you're making these loans is let's say it's the city of Bozeman, since we're located in Bozeman, and we're going to create an imaginary scenario here.

So the [00:10:00] city of Bozeman wants to lend money and they say, you know, if you give us a thousand dollars, 'cause they'll go to the public and do these incremental loans. So they'll say, if you give us a thousand dollars and let us keep it for 10 years, we're going to pay you a thousand dollars back in 10 years.

And that sounds like that'll work pretty well for, you know, keeping your thousand dollars stable. What I'll say is this thousand dollars, 10 years from now, isn't worth what a thousand dollars well by today it's, you know, a movie ticket used to cost and nickel kind of concept.

Christa Hudak: And Matt, what are they using this money for?

Matt Hudak: I don't know, maybe another high school. We could use a third one here in town.

Christa Hudak: Probably.

Matt Hudak: Yeah. So, in return for this, where you're going lend them the money, they're going pay you, let's say $60 a year. Okay? So that's 6% interest. If you're like me and struggle with math from time to time.

So, they're [00:11:00] going pay you $60 a year and that's going continue each of these 10 years until you get your principal back. Well, let's say in two years you want, and I don't know if there are 10 tick marks here, by the way, so don't count that. But if say in two years you need your principal back 'cause you want to buy a car or you want to do something fun, whatever it might be.

Well, if you go to the city of Bozeman at that point in time, they have no obligation to give you your money back. So they might just tell you to kick rocks. In fact, that's kind of generally what happens. So there's a system where if you want your thousand dollars back, you go out to the general market and it's a format.

It looks a lot like Craigslist but existed way longer than Craigslist has. But you go to this system where we post this for sale and then somebody says, yeah, I want that loan, or I don't want that loan. And what happens when you do that is if the city of Bozeman instead of $60 is paying [00:12:00] $80 now, well the person that's going to buy this from you is going to want, you know, to get a little bit of a discount on the price because they can get more interest if they just go straight to the city of Bozeman. And the opposite is also true. If instead of $60, they're paying, you know, $50. Then you're going to call and you're going to know that, then you're going to call the city and find that out, and then you'll end up offering to sell this for a little bit of a profit.

And so these prices, we call these bonds by the way. We try to avoid the jargon when we can. So in this mix, these bonds that these loans that you make move the opposite direction of interest rates. So when interest rates rise, the price of the bond goes down and when interest rates decline, the price of the [00:13:00] bond goes up.

So we believe that these investments work as they are, right? They're great. If you need to get $60 a year and you're fine with the thousand dollars being worth a little bit less because of inflation and ten years from now, that's a phenomenal product. It works really, really well. It's stable. Some of these are secured too against property. That's why there's a little bit of a myth, but that's why bonds are seen as more secure than stocks.

Christa Hudak: And you have a specific contract of how much you're going to get.

Matt Hudak: Yeah. And so you get some protections that can exist within those from default risk and stuff like that.

But within this it works if you're going to own that as an individual investment for that period, and you're comfortable holding it until it matures. A lot of times what we see though is these are held in funds for people and if you have a bond fund in your portfolio, what they're actually doing is they're often trading those bonds so that they can [00:14:00] get some extra yield.

So maybe they can make a profit as interest rates are declining and they have to also create the fund, the money to liquidate and to pay people out when people want to pull money out of their funds. And so there's some functions where a lot of times they're trading these bonds to make a profit rather than owning them for the interest.

And it creates a scenario where it's really almost just as much of a day-to-day fluctuation as the stock market, it's not the same amount of volatility if you measure it in a percent, but it's relative to what you're getting out of the bond. It's actually pretty similar, and they don't necessarily move in an opposite direction when you really need 'em to.

Christa Hudak: Another thing that we frequently see, as Matt discussed earlier when you are evaluating making a loan to somebody, you want to know whether or not they're going to pay you back, and that should impact the interest rate that you're going to get in receiving that if you feel like something's not very likely to pay you back, you might say, hmm, to compensate for this risk, I need a higher rate of return.

And one of the things that we frequently see [00:15:00] as we look at portfolios is where people hold bond funds that are specifically labeled high yield bond funds. And another technical industry term for that is actually junk bonds. And what these are is low quality, below investment grade loans that have a high risk of default and not paying on them.

And so they're able to get a much higher yield and well, sometimes it works well, but there's also a risk that those stop being paid, so they tend to be less secure as well.

Matt Hudak: Yep. And we kind of look at yield as interest rate, and that's another jargon term that we often use and sometimes, or avoid, it's basically like a rate of payout.

So, in this case, it's the interest rate that you receive from the bonds. So the higher the interest that you get, the more risk there is of default and other issues with the bond.

Christa Hudak: So Matt what's the other side and owning businesses?

Matt Hudak: The other side of this is owning businesses. You read my mind. It's underlining it right there. And owning businesses really [00:16:00] this is the function of the stock market. It was what it was designed to do. It was a way for you to own a tiny fraction of a large business and have the right, a lot of the rights of an owner, the rights to vote, rights to profits, all of that from the business.

And so when we look at the stock market, rather than trading the stock market day to day to get price, like price increases and get a capital gain here or there and take profits from it and maybe make money, maybe lose it, rather than treating the markets like a casino, whether that's day to day or on a longer, slightly longer term basis. We look at it as a way to own a business that you would want to own. And you can think about that a lot like owning a taco truck. This is my favorite analogy 'cause I love tacos, but it always makes me hungry. So tacos later! When you're owning a business, and just by the nature of kind of how our industry works, we're not going to talk about the specific companies, not because we're not happy to share how we do this in specific terms, but I don't want to lead you on that. You know, a company we're [00:17:00] going to talk about specifically is a good investment and then a year from now have something change and have you watch this video and then try to replicate what we're talking about and have it not work. So, we're going to talk generically, so you're going to own a business and there are so many of these, think about any of the corporations that you've seen and maybe you can put a placeholder in. When we're looking at this business, they've divided it up and it might be into millions and millions and millions of fractions, and you're going to want to own this little piece of it.

And so the company sells products. Maybe they make deodorant and personal care items or whatever.

Christa Hudak: Or maybe they make tacos.

Matt Hudak: Or maybe they make tacos. And you're going to get a portion of that earnings in the business, they're selling products like tacos. So if you're going to buy this taco truck, right, and let's say you're going to buy the whole thing because it's a taco truck and it's not a major corporation, but you're going to buy the taco truck. What questions are you going to ask?

You're [00:18:00] going to ask, you know, what does it cost to make a taco. What do beans cost? Do I have to hire people to run this or am I going to run this myself? Do I have old debts that I have to pay off? Will I have to finance the taco truck? Do they have a retirement plan where there's going to be obligations coming up? What's kind of the makeup of this? You're also going to ask, do people want tacos?

Matt Hudak: And I think we all know the answer is always, but when we're looking at this, we're going to look at the details of that business. And at the end of the day, no matter how much I love tacos, and hopefully you have a feeling for that at this, at this point, that no matter how much I love tacos, I can't buy the taco truck if it doesn't pay me at the end of the day.

That's the fundamental nature of business ownership is that it has to pay you a paycheck. If it doesn't, I'm better working a real job and going and getting tacos.

Matt Hudak: So from that standpoint, we have to look at these major corporations from that same lens. And when we do [00:19:00] that, it's really shown to work when we test this throughout history with less risk than most other things and more return. And that relationship looks really attractive when we just take the simple approach.

Christa Hudak: When we're looking at businesses in the stock market, one of the things to remember when we talk about risk, we're really talking about these fluctuating values.

And that's really the thing that causes some stress, right? In stock market investing is how much fluctuation do you see? So we always think of it as a good thing when we can get the return that people want to see, but also make those fluctuations less dramatic.

Matt Hudak: Yeah. And so this really works well for it. And not all businesses that you see that are listed on the stock exchange do this. Not all businesses that are listed on the stock exchange even have a profit. You would be amazed at how many companies are actually hemorrhaging money and people are investing and paying more for them, thinking, you know, they're going to be the future someday.

But if you looked at it as a business that you were going to buy to [00:20:00] run yourself, you would turn and run away. It just is not a good business to own and we don't believe in doing those kinds of things. We like to own good businesses. So let's say this business that we're talking about that brings in $3, whether it's a taco truck or

a tech company.

Christa Hudak: $3 for each share.

Matt Hudak: Yep. For each share for each one of these fractions that you might own. So it's bringing in $3 and in that it's going to pay out or we're going to want to see it use a dollar. And this is approximate. Let's say it's going to keep a dollar in reserves because it might need to build a new factory or they might need to do something with it. Create a new product or do research. So they're going to keep a dollar. We want to see that stability going with them. Lots of free cash flow, cash reserves, but they're also going to do something magic, and they're going to pay a dollar out to you as an owner.

Matt Hudak: And we want to see that. If a company doesn't do this, it's a sign that the company's not really mature in its development yet. [00:21:00] And there are a lot of investment arguments where you can say, well, maybe is that spigot? This is a spigot. Yep. There are a lot of arguments that say maybe you can make money on that, but it's not really assured.

Matt Hudak: Like you don't know until it starts coming out. So we're going to put a spigot on here and then what we'll do is we'll say this is paying a dollar, and maybe for the last 80 years this has paid a dollar out to its shareholders or maybe it's increased it for 80 years and has paid it out for a hundred.

We want to see this income coming in consistently and rising. That means market crashes happen. It's probably still coming in.

Unless there's something truly catastrophic with the company. And we can see that hopefully from develop and build from a little ways away if we're looking carefully.

But it's paying a dollar this year and then, you know, next year, because it's always does this, it seems or almost always does this increase, it might pay you a $1.10 and then the next year it's going to pay you a $1.30. That's [00:22:00] actually tangible value to you. You can understand what that is. That's $3 and 30 cents.

Christa Hudak: And Matt, how is this amount that's paid, determined?

Matt Hudak: This is determined as a flat dollar amount by the board of directors of these companies every year. So they sit down and say, we're paying this. It's not a percent. We'll talk about this as a dividend yield. It's what we call it. And it's paid out by the board of directors. So what happens is they don't look at this as a percentage. They look as a flat dollar, and they're going to pay that, and so we hope to see a pretty good dividend on most of the companies that we own. We really like to see about about 3% or so.

Where you get this good consistent income, and that's what gives a business its value. It's the paycheck that you get, and when we're looking at it, we're able to say, you know, this $3 and 30 cents, because it's going to continue and there's a little bit more math than just simply adding it up, but not much.

This gives a business value. It gives us an enough value we can [00:23:00] appraise this business for and say, you know, it's worth it to buy this business. And we might say, this business, we will pay $50 a share is a fair price to pay for that cash flow that we're buying. And knowing that if that continues and that cash flow continues to grow, we might be able to sell it for $55 in a few years.

And that's pretty stable. If it goes up to 70 and skyrockets, we won. If it just kind of plods along, then we're still really happy. And so it gives us the ability to manage this with some reason to believe in it. And if it things go down and the market crashes, and we can probably pull this illustration down now at this point.

So we'll pull this off and just talk to you. When we're looking at this, when the markets go down then, it also mitigates a lot of risk because there's cash coming in. So not only do you have a reason to say this company has a fair market value, even though it's on sale

It's going to continue to be consistently performing over the long term, and we have a good reason to believe that. It also means that we get cash coming [00:24:00] into your portfolio on a day-to-day basis, or on a month to month basis, where that cash that's going to come in is going to be able to buy shares at a lower price or distribute cash where we don't have to sell things at a loss or at a lower value for your cash flow needs.

So it really stabilizes the portfolio too.

Christa Hudak: Yeah, we view this as a great way to provide a lot of stability and also remember that there's a basis for the value of the investments that you hold. We hope that this has been helpful for you as you explore these concepts and look forward to having a conversation with you soon.

Hi everyone! This is my first time sending out an annual market review, and I am excited to share it with you all. As we leave 2025 and enter 2026, we all at CoCreate are feeling energized and hopeful for what’s to come.

Financial markets do not move in straight lines, and 2025 was no exception. While the year had its ups and downs, it also offered valuable lessons about patience and long-term thinking. In this review, we will take a closer look at the key events and major themes of the year, and what we believe matters most moving forward.

As we move into 2026, our focus remains on being thoughtful stewards of your investments. In a year shaped by uncertainty and change, we believe careful decision-making matters more than quick reactions. Markets will always react to headlines, but long-term success comes from staying grounded, patient, and intentional.

Rather than chasing trends, we emphasize diversifying your investments among businesses that are well run, have highly profitable goods and services that people want, and that pay you cash in return for your investment. This approach helps protect portfolios during periods of fluctuation while positioning them to grow over time.

At the end of the day, markets will continue to evolve, headlines will come and go, and uncertainty will always be part of investing. Our role is to help you stay grounded through it all by making thoughtful decisions, staying flexible when needed, and keeping your long-term goals in the center stage. By focusing on what we can control and being wary of what we cannot, we can look forward to the next year with clarity and confidence.

I have gone into more detail below and would be happy to answer any questions you may have.

I hope you have all had a wonderful close to your 2025, and I’m looking forward to meeting with you and having a great 2026 together.

- Emma Shaw

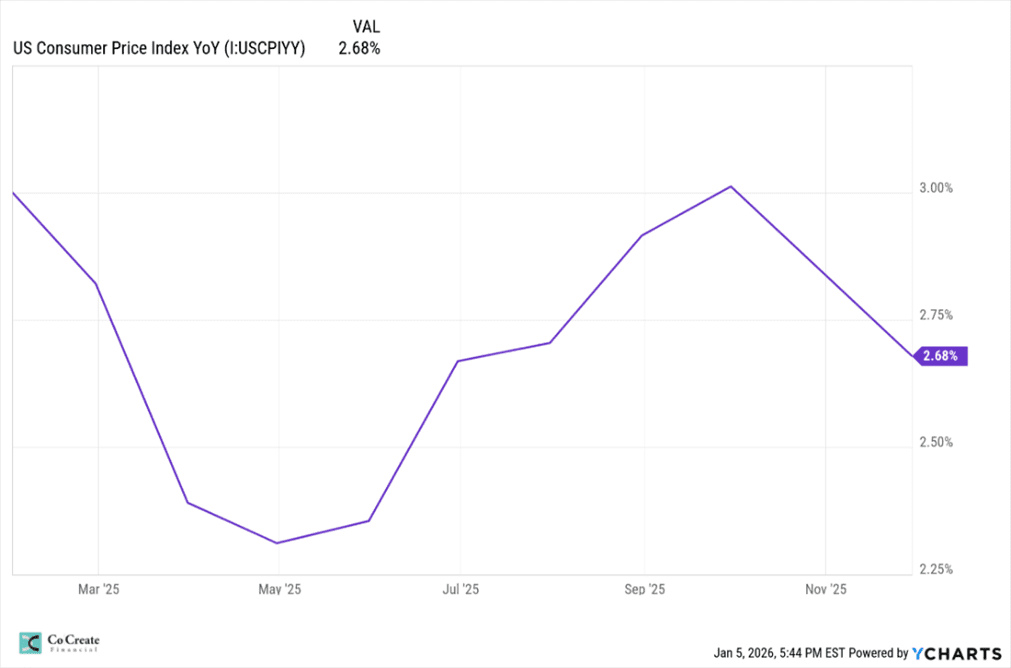

Inflation stayed in the spotlight throughout 2025 as investors and policymakers tried to figure out if rising prices were truly beginning to come under control. The most common way to track how quickly prices are increasing is by looking at the Consumer Price Index (CPI), which measures the cost of everyday items like food, gas, housing, and medical care. When CPI goes up, it means things are getting more expensive, and when CPI goes down, it means price increases are starting to slow.

At the start of 2025, CPI inflation was around 3%, which is higher than the Federal Reserve’s long-term goal of 2%. By the end of the first quarter, inflation cooled to around 2.4%, which was a positive sign that pricing pressures were starting to let up. However, progress was not linear, and CPI moved back up to roughly 2.7% by mid-year and hovered close to 3% again by early fall before going back down below 2.7%.

The graph above tracks CPI inflation over the course of the year. The line moving down means inflation is slowing, while the line moving up means inflation is picking back up. This back-and-forth pattern we can see explains why inflation continued to feel frustratingly “sticky,” even when some areas of the economy improved.

But the uneven path of inflation in 2025 is not a complete surprise, inflation rarely dissipates quickly, and expecting a smooth decline is not totally realistic. It’s normal for progress to stall or even reverse temporarily, especially when wages and housing costs remain elevated.

For investors, this backs up the importance of remaining patient and not overreacting to shorter-term data. The stabilization process is complex, made up of many various interlocking elements that move at different paces.

This graph depicts the U.S. inflation rate over the past three years. The broader trend still points towards gradual improvement, and we can navigate the uncertainty by remaining diversified, focusing on fundamentals, and avoiding emotional decisions based on fleeting headlines.

Throughout 2025, central banks, led by the Federal Reserve, took a cautious approach to interest rate decisions. After raising interest rates aggressively in prior years to fight inflation, policymakers shifted towards a slower, more thoughtful strategy.

Interest rates deal with the cost of borrowing money. When rates go up, loans become more expensive and spending tends to slow. When rates go down, loans become cheaper and spending increases. One of the Federal Reserve’s duties is to adjust rates to help keep inflation under control while also supporting economic growth.

Since inflation moved up and down during the year, expectations surrounding possible rate cuts were inconsistent. At times, investors expected rates to fall sooner, but when inflation readings came in higher, the Fed signaled it was willing to wait to make a move until they had a more complete picture.

Federal Reserve Chair Jerome Powell repeatedly emphasized that decisions would depend on clear progress in the data, not on what markets hoped would happen. The Fed needed tangible proof that inflation was improving.

On December 10, the Fed lowered interest rates by 25 basis points, which equals 0.25%. This was the third rate cut of the year. These small cuts suggest growing confidence that inflation is moving in the right direction, but again, these things take time and rate cuts do not bring change overnight.

Even as inflation started to cool, borrowing money remained expensive throughout much of 2025. Mortgage rates remained high, adding to the slower activity in the housing market and affecting affordability for buyers and refinancers. Higher monthly payments made homes less affordable, and fewer people chose to refinance their existing mortgages. This kept many buyers on the sidelines and reduced overall housing demand.

The chart above tracks the 30-year fixed mortgage rate, which is the most common home loan in the U.S. The line shows how mortgage rates moved throughout the year. When the line goes down, borrowing becomes slightly cheaper. When it stays high, monthly payments remain a challenge for buyers.

Although mortgage rates declined some towards the end of the year, they remained well above the low levels we’ve seen in other years, finishing around 6.15%. While this drop offered some relief, rates were still high enough to limit affordability for many households.

Higher interest rates also affected businesses. Companies faced higher financing costs, which made them more cautious about expanding, hiring, and investing in new projects. For consumers, borrowing became more expensive across credit cards, auto loans, and personal loans, making everyday purchases harder to finance and encouraging households to be more selective with spending.

Mortgage rates will take longer to come down, even if the Federal Reserve continues to cut interest rates. While rate cuts help lower short-term borrowing costs, mortgage rates are influenced by more than just Fed policy. Meaningful relief for homebuyers will require steady improvement in inflation and economic stability over time.

Interest rate movements had a broad impact on markets in 2025. Bond prices moved as rate expectations shifted. When interest rates stay high, existing bonds lose value, but new bonds offer higher yields, meaning better income potential going forward.

Stocks also experienced periods of volatility throughout the year. Higher interest rates make borrowing more expensive for companies and reduce the value of their future earnings, which can put pressure on stock prices. As investors adjusted to these conditions, markets reacted more sharply to economic data and rate expectations.

Despite short term swings, the higher-rate environment reinforced the importance of diversification. Balanced portfolios tended to perform more steadily, as income-generating assets played a larger role and helped offset equity volatility.

Economic growth in 2025 was more resilient than many early forecasts suggested. While higher interest rates were expected to significantly slow down activity, overall GDP growth remained positive, though more moderate than in prior years. GDP is a simple way to measure the health of the economy. It represents the total value of all goods and services produced in a country over a certain period. On the one hand, the U.S. economy continued to expand at a steady pace rather than experiencing any sharp contractions, showing its ability to adapt to tighter financial conditions. On the other hand, AI investment was responsible for approximately 92% of GDP growth in 2025 and tariffs appear to be costing about 1% of GDP.

As we can see in the graph above, which measures U.S. GDP throughout 2025, the slower pace of growth suggests the economy is settling into a healthier balance. Instead of growing too fast or slowing down too much, businesses and consumers adjusted their spending and investment decisions at a more sustainable pace.

The job market remained relatively stable throughout the year, though hiring slowed compared to the rapid pace seen in recent years. According to the Bureau of Labor Statistics (BLS), total employment continued to grow, particularly in areas like health care and service-related jobs. The unemployment rate, which measures the number of people actively looking for work but unable to find it, edged slightly higher but remained near normal historical levels. This leads to a cooling job market rather than a major slowdown. As I’ve mentioned before, employers just became more selective with hiring as interest rates stayed high and economic growth softened. One notable change was a 9.2% decline in federal government employment, as hiring slowed and some government roles were reduced. This contributed to the overall deceleration of job growth.